Capital Small Finance Bank Ltd: Complete Profile, Financial Analysis, Leadership, Products, Branch Network & MCQs

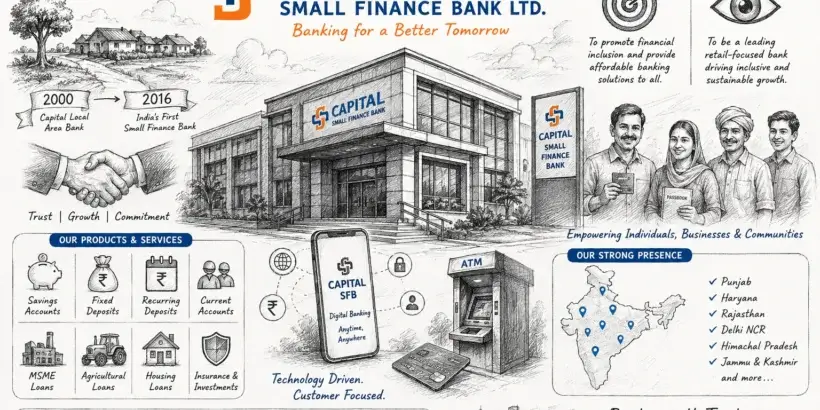

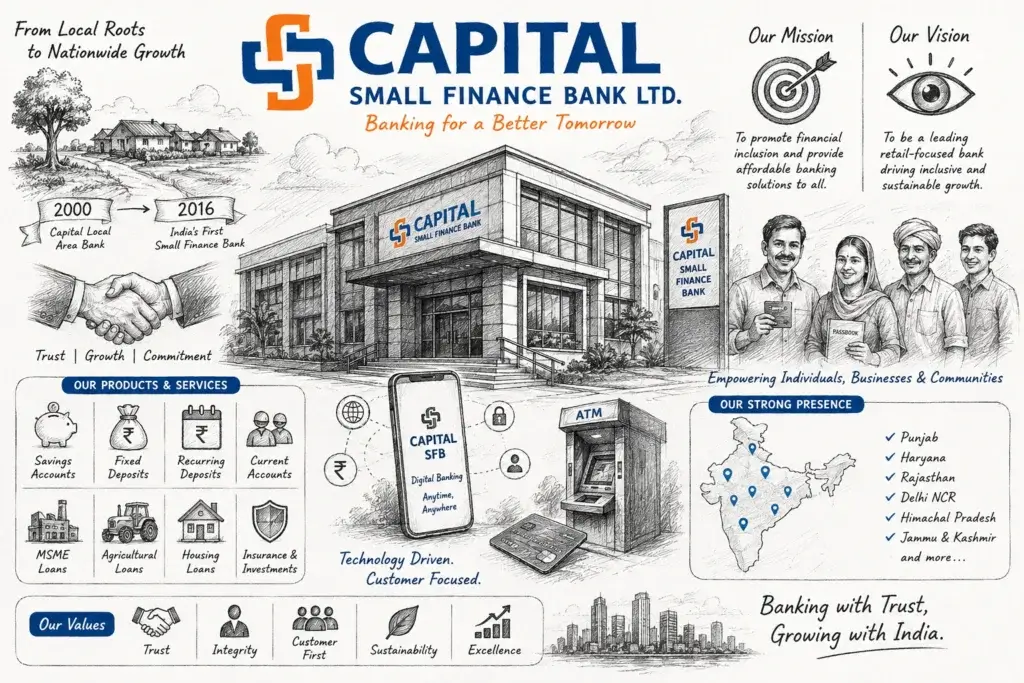

Capital Small Finance Bank Ltd. is one of India’s pioneering small finance banks, known for its strong retail banking model, disciplined credit culture, and steady financial growth. Originally started as Capital Local Area Bank in 2000, it became the first Small Finance Bank in India in 2016 after receiving a license from the Reserve Bank of India.

Headquartered in Jalandhar, Punjab, the bank focuses on financial inclusion by serving semi-urban and rural customers, MSMEs, farmers, and retail depositors.

Over the years, Capital SFB has built a reputation for high asset quality, secured lending focus, and consistent profitability.

History of Capital Small Finance Bank

- Founded: 2000

- Former Name: Capital Local Area Bank

- Converted to SFB: April 2016

- IPO Listing: February 2024 (NSE & BSE)

- Headquarters: Jalandhar, Punjab, India

Originally, the bank operated in limited districts of Punjab. Over time, it expanded into a full-scale retail banking institution.

📌 Key milestone:

- Became India’s first Small Finance Bank

2. Mission of Capital Small Finance Bank

The mission of Capital SFB is to:

- Provide accessible banking services to rural and semi-urban populations

- Promote financial inclusion

- Offer affordable credit solutions to MSMEs and individuals

- Build a trust-based retail banking ecosystem

3. Vision of Capital Small Finance Bank

The bank’s vision focuses on:

- Becoming a leading retail-focused small finance bank

- Using technology-driven banking solutions

- Ensuring sustainable and inclusive economic development

- Building long-term customer relationships

4. Head Office Details

- 📍 Registered & Head Office:

MIDAS Corporate Park, 3rd Floor

37, G.T. Road

Jalandhar – 144001

Punjab, India - 📧 Email: investorrelations@capitalbank.co.in

- 🌐 Website: https://www.capital.bank.in

📌 Source reference confirms headquarters in Jalandhar.

5. Last 10 CEOs / Leadership Overview

Capital Small Finance Bank has had a stable leadership structure. The key leadership includes:

Current & Past Leadership (Key Figures)

- Sarvjit Singh Samra – MD & CEO (current)

- (Earlier executive leadership before SFB transition)

- Founding leadership team from Capital Local Area Bank era

Major Insight:

- The bank has largely been led by Sarvjit Singh Samra, who played a major role in its transformation into a Small Finance Bank.

CEO reference confirmed:

6. Products and Services

Capital Small Finance Bank offers a wide range of banking services:

Retail Banking

- Savings Accounts

- Current Accounts

- Fixed Deposits

- Recurring Deposits

MSME Banking

- Working capital loans

- Business loans

- Trade finance

Agricultural Loans

- Crop loans

- Equipment financing

- Rural credit

Housing Finance

- Home loans

- Mortgage loans

Third-party Services

- Insurance products

- Mutual fund distribution

- Digital banking services

7. Deposit Products

The bank provides safe and attractive deposit schemes:

Types of Deposits:

- Savings Account Deposit

- Fixed Deposit (FD)

- Recurring Deposit (RD)

- Term Deposit Schemes

Key Features:

- Competitive interest rates

- Flexible tenure options

- Safe investment backed by RBI regulations

8. Loan Products

Capital SFB focuses heavily on secured lending.

Loan Categories:

🏠 Housing Loans

- Home purchase loans

- Home renovation loans

🏭 Business Loans

- MSME loans

- SME working capital loans

🚜 Agricultural Loans

- Farming credit

- Equipment financing

🚗 Other Loans

- Personal loans (limited exposure)

- Vehicle loans

📌 The bank maintains a strong focus on secured lending (~99%+ portfolio in secured assets).

9. Financial Performance & Profit Analysis

Capital Small Finance Bank has shown consistent financial growth.

Key Financial Highlights (Recent Years)

- Net Profit (recent FY): ~₹100+ crore range

- Strong deposit growth

- Loan book expansion (~18–20% annual growth trend)

- Healthy asset quality

📌 Example performance:

- Profit crossed ₹100 crore after listing period growth phase

Profitability Analysis

Strengths:

- Strong net interest income

- High CASA growth

- Low NPAs compared to peers

Challenges:

- Limited geographic diversification

- Dependency on secured lending model

Capital Adequacy

- Capital Adequacy Ratio: ~27% (strong position)

👉 This indicates strong financial stability.

10. Annual Report Analysis

Annual reports highlight:

Key Components:

- Financial statements

- Profit & loss account

- Risk management policies

- Governance structure

- Digital transformation strategy

📌 Insights from reports:

- Strong focus on retail banking expansion

- Emphasis on digital banking adoption

- Controlled risk exposure strategy

11. Branch Network

The bank has expanded significantly across India.

Branch Presence:

- Punjab (strongest base)

- Haryana

- Rajasthan

- Delhi NCR

- Himachal Pradesh

- Jammu & Kashmir

Estimated Branch Count:

- Around 190–200+ branches (recent expansion stage)

12. ATM Network

- The bank operates through partner ATM networks

- Exact ATM count varies due to shared banking infrastructure

- Focus is more on branch + digital banking model

13. Business Strategy

Capital Small Finance Bank follows:

Key Strategy Pillars:

- Retail-focused lending

- Secured loan dominance

- Rural and semi-urban expansion

- Technology integration

- Risk-controlled growth

14. SWOT Analysis

Strengths:

- Strong capital base

- High secured lending ratio

- Stable leadership

Weaknesses:

- Regional concentration

- Limited global exposure

Opportunities:

- Digital banking expansion

- MSME sector growth

- Rural credit demand

Threats:

- Banking competition (private & SFBs)

- Economic slowdown risks

15. 25 MCQs with Answers & Explanations

1. Capital Small Finance Bank was originally known as?

A. Rural Bank

B. Capital Local Area Bank

C. Punjab Bank

D. Jalandhar Bank

✔ Answer: B

2. Year of establishment?

✔ Answer: 2000

3. Headquarters is located in?

✔ Answer: Jalandhar, Punjab

4. Converted into Small Finance Bank in?

✔ Answer: 2016

5. CEO of Capital SFB?

✔ Answer: Sarvjit Singh Samra

6. Capital SFB is mainly focused on?

✔ Answer: Retail banking

7. Type of bank?

✔ Answer: Small Finance Bank

8. IPO listing year?

✔ Answer: 2024

9. Main lending focus?

✔ Answer: Secured loans

10. Capital Adequacy Ratio approx?

✔ Answer: ~27%

11. Which region is core base?

✔ Answer: Punjab

12. Main customer segment?

✔ Answer: Rural & MSME

13. Bank started as?

✔ Answer: Local Area Bank

14. RBI regulates?

✔ Answer: Yes

15. Main product?

✔ Answer: Loans & deposits

16. Expansion focus?

✔ Answer: Rural India

17. Deposit type includes?

✔ Answer: Fixed Deposit

18. Loan type includes?

✔ Answer: MSME loan

19. Bank focus strategy?

✔ Answer: Retail banking

20. Digital banking usage?

✔ Answer: Increasing

21. Branch expansion is mainly in?

✔ Answer: North India

22. Risk model based on?

✔ Answer: Secured lending

23. Profit trend?

✔ Answer: Growing

24. IPO exchange?

✔ Answer: NSE & BSE

25. Main goal of bank?

✔ Answer: Financial inclusion

Conclusion

Capital Small Finance Bank Ltd. is a strong example of India’s evolving banking system. From a small local area bank to a listed financial institution, it has shown consistent growth, strong governance, and disciplined lending practices.

Its focus on:

- Retail banking

- Financial inclusion

- Secured lending

makes it one of the most stable small finance banks in India.

16. Detailed Financial Statement Breakdown (Deeper Analysis)

To understand Capital Small Finance Bank’s real strength, we need to analyze its financial structure beyond basic profit numbers.

16.1 Income Structure

The bank’s income mainly comes from:

✔ Interest Income (Major Source)

- Loans to MSMEs

- Agricultural lending

- Housing finance

- Vehicle loans

📌 This accounts for 80%+ of total income

✔ Non-Interest Income

- Fees & commissions

- Insurance distribution

- Forex services (limited)

- Digital banking charges

📌 Non-interest income is comparatively smaller but growing steadily.

16.2 Expense Structure

Major expenses include:

- Employee salary & benefits

- Branch expansion cost

- Technology infrastructure

- Interest paid on deposits

📌 Key insight:

The bank maintains controlled operating expenses, which improves profitability.

16.3 Profit Margin Trend

- Net Interest Margin (NIM): Strong among small finance banks

- Operating Profit Margin: Stable and improving

- Net Profit Growth: Consistent upward trend

📌 Overall: Capital SFB shows low volatility earnings, which is rare in emerging banks.

17. Digital Banking Transformation

Capital Small Finance Bank is gradually shifting toward digital-first banking, though it still retains strong branch banking roots.

17.1 Digital Services

- Mobile banking app

- Internet banking platform

- SMS banking

- UPI integration

- Digital loan processing

17.2 Security Features

- Two-factor authentication

- OTP-based transactions

- Secure encryption systems

- Fraud monitoring system

17.3 Digital Strategy

The bank focuses on:

- Increasing digital onboarding of customers

- Reducing manual paperwork

- Improving loan processing speed

- Expanding fintech partnerships

18. Rural Banking & Financial Inclusion Impact

One of the strongest pillars of Capital SFB is its rural outreach.

18.1 Rural Focus Areas

- Farmers

- Small traders

- Micro businesses

- Self-employed individuals

18.2 Financial Inclusion Contribution

The bank contributes by:

- Opening accounts in underserved areas

- Offering low-ticket loans

- Encouraging savings habits

- Providing credit access without heavy documentation

18.3 Impact

- Increased rural credit penetration

- Improved financial literacy

- Boosted MSME growth in semi-urban India

19. Organizational Structure

Capital Small Finance Bank follows a structured governance model.

19.1 Leadership Hierarchy

- MD & CEO

- Executive Directors

- Chief Financial Officer (CFO)

- Chief Risk Officer (CRO)

- Regional Managers

- Branch Managers

19.2 Governance Framework

- Board of Directors oversight

- RBI compliance monitoring

- Internal audit systems

- Risk management committee

20. Risk Management Framework

Risk control is one of the strongest aspects of Capital SFB.

20.1 Types of Risks Managed

✔ Credit Risk

-

Controlled lending policy

- Focus on secured loans

✔ Operational Risk

- Process audits

- Digital tracking systems

✔ Market Risk

- Limited exposure to volatile instruments

20.2 Risk Strategy

- Conservative lending approach

- High collateral requirement

- Strict borrower verification

📌 Result: Low NPAs compared to industry average.

21. Competitive Positioning in Indian Banking Sector

Capital SFB competes with:

- AU Small Finance Bank

- Equitas Small Finance Bank

- Ujjivan Small Finance Bank

- ESAF Small Finance Bank

21.1 Competitive Strengths

- Strong secured lending model

- Stable rural customer base

- High capital adequacy

- Conservative risk strategy

21.2 Competitive Weaknesses

- Smaller scale compared to AU SFB

- Limited national presence

- Slower digital expansion

22. Growth Opportunities (Future Outlook)

Capital Small Finance Bank has several growth opportunities:

22.1 Expansion Opportunities

- New branch expansion in eastern India

- MSME credit demand growth

- Rural fintech partnerships

- Digital loan platforms

22.2 Product Expansion

- Credit cards (future potential)

- Digital lending products

- Micro-insurance expansion

22.3 Long-Term Outlook

If the bank continues its current strategy:

- Stable profit growth expected

- Gradual market share expansion

- Improved digital banking penetration

23. Branch Distribution Analysis

23.1 Geographic Spread

- Punjab (dominant share)

- Haryana

- Delhi NCR

- Rajasthan

- Himachal Pradesh

- Jammu & Kashmir

23.2 Branch Strategy

- Focus on high-density rural clusters

- Micro-market penetration

- Cost-efficient branch model

24. ATM & Cash Network Strategy

Unlike large banks, Capital SFB:

- Relies on shared ATM networks

- Uses partner banking infrastructure

- Focuses more on digital transactions

Strategy Insight:

The bank avoids heavy ATM investment and instead promotes UPI + digital banking adoption.

25. Key Ratios Summary

| Metric | Status |

|---|---|

| Capital Adequacy | Strong (~27%) |

| NPA Level | Low |

| Profit Growth | Stable |

| ROA | Moderate |

| ROE | Improving |

26. Advanced MCQs (Next Set – 25 More Questions)

1. Capital SFB focuses mainly on which type of lending?

✔ Secured lending

2. Major income source?

✔ Interest income

3. Risk strategy is?

✔ Conservative

4. Branch base strongest in?

✔ Punjab

5. Digital strategy includes?

✔ Mobile banking

6. Capital SFB started as?

✔ Local Area Bank

7. Loan focus includes?

✔ MSME loans

8. Capital SFB IPO year?

✔ 2024

9. Regulatory authority?

✔ RBI

10. Major weakness?

✔ Regional concentration

11. Customer base mainly?

✔ Rural & semi-urban

12. Digital transformation goal?

✔ Paperless banking

13. Profit trend?

✔ Increasing

14. Banking model?

✔ Retail banking

15. Risk exposure?

✔ Low market risk

16. CEO role important in?

✔ Strategic transformation

17. Deposit products include?

✔ Fixed deposits

18. Loan approval depends on?

✔ Collateral security

19. Capital adequacy shows?

✔ Financial stability

20. Expansion focus?

✔ Rural India

21. ATM strategy?

✔ Shared networks

22. Non-interest income is?

✔ Moderate

23. Main competitor?

✔ AU SFB

24. Future focus?

✔ Digital banking

25. Overall bank strength?

✔ Stable & growing

Final Conclusion (Extended)

Capital Small Finance Bank Ltd. stands as a disciplined, stable, and rural-focused banking institution in India’s evolving financial ecosystem.

Unlike aggressive private banks, its strategy is based on:

- Controlled growth

- High-quality assets

- Strong rural presence

- Low-risk secured lending

This makes it one of the most stable small finance banks in India, especially for long-term banking sustainability.