Automatic Teller Machine (ATM): Complete Guide, History, Functions, Benefits, Features, Security, and Future of ATM Banking

An Automatic Teller Machine (ATM) is one of the most important innovations in modern banking. It allows customers to perform various banking transactions without visiting a bank branch or interacting with a bank employee. ATMs provide quick, convenient, and secure access to banking services at any time of the day or night.

In today’s fast-paced world, people expect banking services to be available whenever they need them. The ATM fulfills this expectation by allowing customers to withdraw cash, check account balances, transfer funds, deposit money, pay bills, and perform many other banking functions 24 hours a day, 365 days a year.

The invention of the ATM revolutionized the banking industry by reducing customer waiting times, decreasing operational costs for banks, and improving customer satisfaction. Today, millions of ATMs operate worldwide, serving billions of transactions annually.

This article provides a comprehensive overview of ATMs, including their history, components, functions, benefits, security features, operating procedures, advantages, disadvantages, and future developments.

What is an Automatic Teller Machine (ATM)?

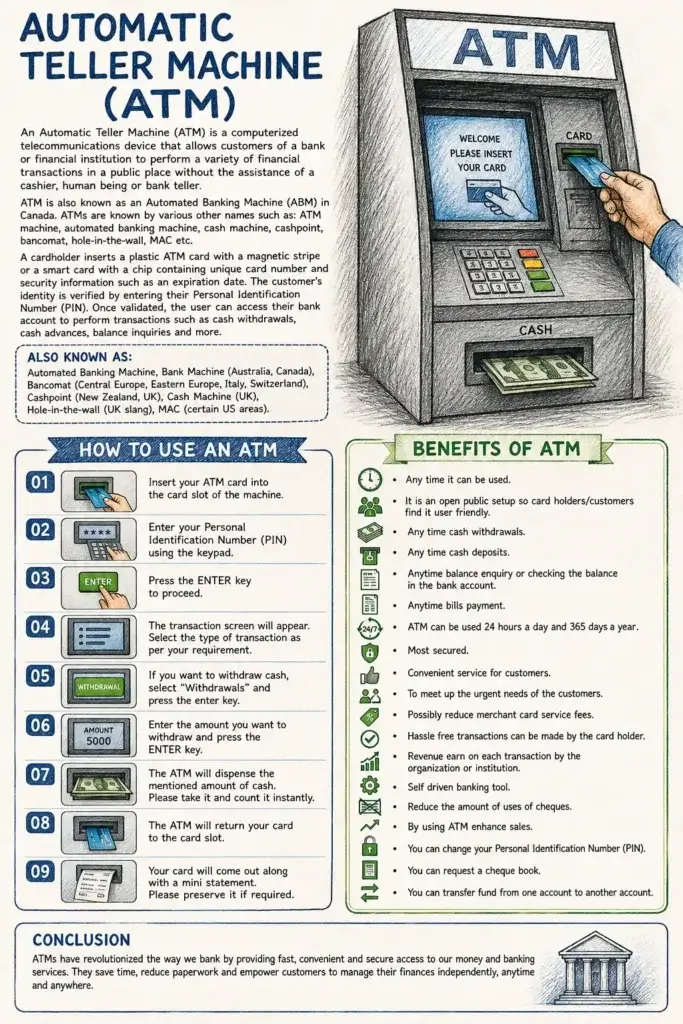

An Automatic Teller Machine (ATM) is a computerized electronic banking device that enables customers of financial institutions to conduct financial transactions without the assistance of a bank teller or cashier.

Customers access ATM services using a debit card, ATM card, credit card, or smart card. Authentication is typically completed by entering a Personal Identification Number (PIN), ensuring that only authorized users can access the account.

The ATM is connected to the bank’s central computer system through a secure telecommunications network. This connection allows the machine to verify customer information and process transactions instantly.

Meaning of ATM

ATM stands for:

A – Automatic

T – Teller

M – Machine

The term “Automatic Teller Machine” refers to a machine that performs many of the functions traditionally carried out by a human bank teller.

Other Names of ATM Around the World

ATMs are known by different names in different countries:

-

Automated Banking Machine (ABM) – Canada

-

Bank Machine – Australia and Canada

-

Cash Machine – United Kingdom

-

Cashpoint – United Kingdom and New Zealand

-

Bancomat – Italy and several European countries

-

Hole-in-the-Wall – Informal British term

-

MAC (Money Access Center) – Certain areas of the United States

Although the names differ, the purpose remains the same: providing convenient self-service banking.

History of the ATM

The ATM is considered one of the greatest technological innovations in banking.

Early Development

The idea of automated banking emerged during the 1960s when banks sought ways to provide customer services beyond normal business hours.

The world’s first modern ATM was installed in London, United Kingdom, in 1967 by Barclays Bank. The machine was developed by John Shepherd-Barron, who is often credited as one of the inventors of the ATM.

Initially, ATMs used paper vouchers rather than plastic cards. As technology evolved, magnetic stripe cards and PIN-based authentication became standard.

Global Expansion

During the 1970s and 1980s, ATMs spread rapidly across Europe, North America, and Asia. Banks recognized that ATM networks could significantly reduce operational costs while improving customer convenience.

Today, ATMs are available in:

-

Banks

-

Shopping malls

-

Airports

-

Railway stations

-

Universities

-

Hospitals

-

Hotels

-

Supermarkets

-

Fuel stations

Modern ATMs now support advanced functions beyond simple cash withdrawal.

Main Components of an ATM

An ATM consists of several hardware and software components.

1. Card Reader

The card reader reads information stored on the ATM card’s magnetic stripe or chip.

2. Display Screen

The screen provides instructions and displays transaction information.

3. Keypad

The keypad allows customers to enter their PIN and transaction details.

4. Cash Dispenser

This component stores and dispenses cash to customers.

5. Receipt Printer

The printer provides transaction receipts and mini statements.

6. Deposit Slot

Some ATMs include a deposit slot for cash and cheque deposits.

7. Security Camera

CCTV cameras monitor ATM activity to enhance security.

8. Communication System

The ATM communicates with the bank’s central server through secure telecommunications networks.

How Does an ATM Work?

ATMs work through a secure connection between the machine and the bank’s central database.

The process typically involves:

-

Card insertion

-

PIN verification

-

Transaction selection

-

Bank authorization

-

Transaction processing

-

Cash dispensing or service completion

-

Receipt generation

-

Card return

The entire process usually takes less than one minute.

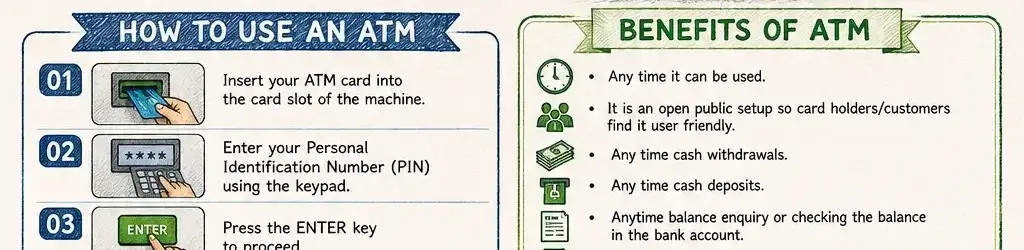

How to Use an ATM

Using an ATM is simple and convenient.

Step 1: Insert Your ATM Card

Insert your ATM card into the card slot according to the instructions displayed on the machine.

Step 2: Select Language

Choose your preferred language from the available options.

Step 3: Enter PIN

Carefully enter your Personal Identification Number (PIN).

Step 4: Press Enter

Press the “Enter” button to continue.

Step 5: Choose Transaction Type

Select the service you require:

-

Cash Withdrawal

-

Balance Inquiry

-

Cash Deposit

-

Fund Transfer

-

Mini Statement

-

PIN Change

Step 6: Enter Amount

If withdrawing cash, enter the desired amount.

Step 7: Confirm Transaction

Review the transaction details and confirm.

Step 8: Collect Cash

Take the cash dispensed by the ATM.

Step 9: Take Receipt

Collect the transaction receipt if required.

Step 10: Remove Card

Always remove your ATM card before leaving.

Types of ATM Transactions

Modern ATMs support various banking services.

Cash Withdrawal

The most common ATM service allows customers to withdraw money from their accounts.

Balance Inquiry

Customers can instantly check account balances.

Mini Statement

ATMs can provide summaries of recent transactions.

Cash Deposit

Many modern ATMs accept cash deposits directly.

Cheque Deposit

Some ATMs allow customers to deposit cheques.

Fund Transfer

Customers can transfer funds between accounts.

PIN Change

Users can update their ATM PIN for security purposes.

Bill Payment

Utility bills and other payments can be made through ATMs.

Mobile Recharge

Many ATMs support mobile phone top-ups.

Benefits of ATM

ATMs provide numerous benefits for customers and financial institutions.

1. 24/7 Availability

ATMs operate twenty-four hours a day and seven days a week.

2. Convenience

Customers can perform banking transactions anytime.

3. Faster Service

Transactions take only a few minutes.

4. Reduced Waiting Time

Customers avoid long queues at bank branches.

5. Easy Cash Access

Cash is available whenever needed.

6. Enhanced Customer Satisfaction

Convenient banking improves customer experience.

7. Secure Transactions

PIN verification and encryption enhance security.

8. Multiple Banking Services

ATMs provide various financial services in one place.

9. Lower Banking Costs

Banks save money by reducing dependence on human tellers.

10. Global Accessibility

International ATM networks allow access to funds worldwide.

Advantages of ATM for Banks

Banks also benefit significantly from ATM technology.

Reduced Operating Costs

ATMs reduce staffing requirements and administrative expenses.

Increased Efficiency

Routine transactions are automated.

Improved Customer Service

Banks can serve customers beyond normal business hours.

Higher Transaction Volume

ATMs handle large numbers of transactions efficiently.

Expanded Market Reach

Banks can provide services in remote areas.

ATM Security Features

Security is a critical aspect of ATM operations.

Personal Identification Number (PIN)

The PIN acts as the primary authentication method.

Chip Technology

EMV chip cards provide stronger protection than magnetic stripe cards.

Encryption

Sensitive information is encrypted during transmission.

CCTV Surveillance

Most ATMs are monitored by security cameras.

Transaction Monitoring

Banks continuously monitor suspicious activities.

Card Blocking

Lost or stolen cards can be blocked immediately.

ATM Safety Tips

Customers should follow these safety guidelines:

-

Keep your PIN confidential.

-

Never share your ATM card.

-

Cover the keypad while entering your PIN.

-

Avoid suspicious ATMs.

-

Check for card skimming devices.

-

Use well-lit ATM locations.

-

Collect your card and receipt.

-

Monitor account statements regularly.

-

Report suspicious transactions immediately.

Common ATM Frauds

Although ATMs are generally secure, fraud can occur.

Card Skimming

Criminals install devices that steal card information.

Shoulder Surfing

Fraudsters observe customers entering PINs.

Card Trapping

Devices trap cards inside the ATM.

Fake Keypads

Fake keypads record PIN entries.

Phishing Attacks

Customers may be tricked into revealing banking details.

Awareness and vigilance help prevent ATM fraud.

Limitations of ATM

Despite many advantages, ATMs have certain limitations.

-

Cash withdrawal limits

-

Technical failures

-

Network outages

-

Security risks

-

Limited complex banking services

-

Maintenance costs

These limitations are generally outweighed by the convenience provided.

Future of ATM Technology

ATM technology continues to evolve.

Future innovations include:

-

Biometric authentication

-

Facial recognition

-

Cardless withdrawals

-

Mobile wallet integration

-

Artificial Intelligence support

-

Contactless transactions

-

Enhanced cybersecurity

-

Voice-assisted ATM services

These developments will make ATM banking even more secure and convenient.

Conclusion

The Automatic Teller Machine (ATM) has transformed the banking industry by providing customers with convenient, fast, and secure access to financial services. From simple cash withdrawals to advanced banking transactions, ATMs have become an essential part of modern financial infrastructure.

Their ability to operate 24 hours a day, 365 days a year makes them invaluable to customers worldwide. Despite challenges such as fraud and technical issues, ongoing technological advancements continue to improve ATM security and functionality.

As digital banking evolves, ATMs will remain a critical bridge between traditional banking and modern financial technology, offering customers reliable access to banking services whenever and wherever they are needed.