Bangladesh Bank: Steering the Nation’s Economic Course

Bangladesh Bank’s Vital Economic Role

Bangladesh Bank, as the central bank of Bangladesh, plays an indispensable role in safeguarding the nation’s financial stability and fostering its economic growth. We recognize its critical responsibility in managing monetary policy, overseeing the banking sector, and shaping the country’s economic future. From stabilizing inflation and managing the national currency, the Taka, to promoting financial inclusion and modernizing banking infrastructure, Bangladesh Bank’s multifaceted functions are central to the nation’s development and global financial integration.

Genesis and Core Responsibilities

Bangladesh Bank was established on December 16, 1971, with retrospective effect, immediately after Bangladesh gained independence. It was formally reorganized under the Bangladesh Bank Order (P.O. No. 127 of 1972) in April 1972, taking over the capital and liabilities of the Dhaka branch of the State Bank of Pakistan. Today, it is fully owned by the Government of Bangladesh.

The central bank’s vision is to continuously evolve as a forward-looking institution with competent and committed professionals, dedicated to monetary management and financial sector supervision. Our mission focuses on maintaining price stability, ensuring financial system robustness, and supporting broad-based, inclusive economic growth, employment generation, and poverty eradication in Bangladesh.

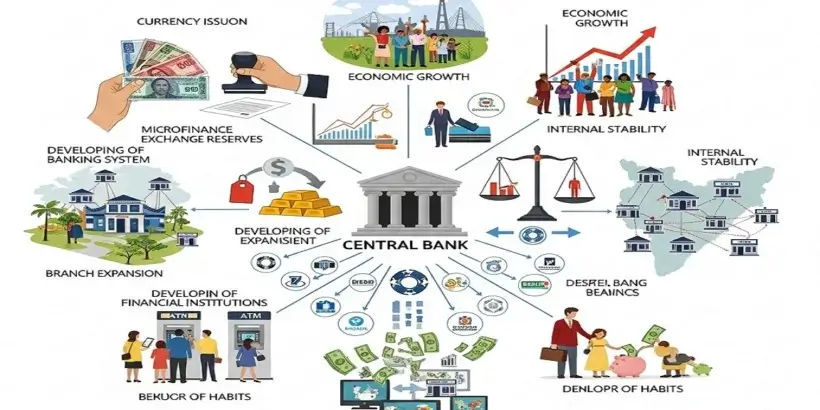

The core functions of Bangladesh Bank are extensive and crucial for a healthy economy:

-

Monetary Policy Formulation and Implementation: Bangladesh Bank is responsible for formulating and implementing monetary policy to stabilize the domestic monetary value and maintain a competitive external value of the Taka. This involves adjusting interest rates and managing the money supply to influence inflation, employment, and overall economic growth. The policy rate currently stands at 10.0%, unchanged since October 2024, with a revised inflation target of “below 8.0%” for FY26.

-

Currency Issuance and Management: We manage the nation’s currency, the Taka, and its interaction with global currencies. This includes issuing currency notes and regulating the foreign exchange market to ensure the Taka’s stability in international markets, which is vital for the country’s export-driven economy.

-

Financial Regulation and Supervision: Bangladesh Bank regulates and supervises scheduled banks and non-bank financial institutions (NBFIs) through off-site and on-site supervision. This is to enhance the safety, soundness, and stability of the banking system, ensure banking discipline, protect depositors’ interests, and maintain confidence in the financial system.

-

Management of Foreign Exchange Reserves: The central bank holds and manages the official foreign exchange reserves, ensuring they are sufficient to cover import needs and external debt obligations. This function is critical for determining currency rates and preventing unexpected inflation.

-

Banker to the Government: Bangladesh Bank acts as the government’s banker, maintaining government accounts and funds, and advising the government on various economic matters.

-

Lender of Last Resort: We serve as a lender of last resort to commercial banks during times of financial crisis, providing liquidity to ensure the stability of the banking sector.

-

Payment System Regulation and Promotion: Bangladesh Bank promotes, regulates, and ensures a secure and efficient payment system, including the issue of banknotes and facilitating inter-bank payments through clearing houses.

-

Financial Inclusion: A significant focus is placed on promoting financial inclusion, encouraging banking services for underserved populations, and supporting digital payment solutions and mobile banking initiatives.

Key Economic Challenges and Policy Responses

Bangladesh’s economy has faced significant challenges in recent years, prompting Bangladesh Bank to implement various policy responses. These challenges include persistently high inflation, a depreciating exchange rate, dwindling foreign exchange reserves, and a growing number of non-performing loans (NPLs) within the banking sector.

Inflationary Pressures

-

Challenge: High and rising prices of essential commodities, particularly food, have been a constant challenge. In July 2024, general inflation significantly increased to 11.66%, with food inflation reaching a record high of 14.10%. This eroded consumer purchasing power, leading to a persistent decline in real wages since mid-2022.

-

Policy Response: To rein in inflation, Bangladesh Bank has consistently tightened monetary policy. This includes introducing an interest targeting framework in FY23 and maintaining a tight monetary condition with a positive real policy rate. The policy rate was maintained at 10.0% since October 2024. Fiscal consolidation efforts, such as expenditure restraint, have also complemented monetary tightening.

Foreign Exchange Reserves and Exchange Rate Volatility

-

Challenge: The country has experienced a decline in foreign exchange reserves and a depreciating Taka, exacerbated by global financial tightening and high international commodity prices. The balance of payments deficit widened, with a significant financial account deficit.

-

Policy Response: Bangladesh Bank has implemented bold exchange rate reforms, including a smooth transition to a flexible exchange rate regime, to address these pressures. We have also tightened control on import flows to manage the reserve decline, although this can impact growth and revenue collection. Efforts are underway to bolster foreign exchange reserve buffers.

Banking Sector Vulnerabilities and Non-Performing Loans (NPLs)

-

Challenge: The banking sector has been struggling with deep-rooted problems, including systemic inefficiencies, weak governance, and a massive accumulation of non-performing loans. Politically motivated appointments, weak internal controls, and ineffective risk management have contributed to these issues. NPLs reportedly rose to around 36% in September 2025, partly due to stricter loan classification rules.

-

Policy Response: Bangladesh Bank has proposed bank mergers and introduced a Prompt Corrective Action (PCA) framework to address these vulnerabilities. We have also taken significant steps, such as dissolving and reconstituting boards of weak banks, undertaking asset quality reviews (AQRs), and initiating mergers of financially distressed institutions. Furthermore, a directive effective from January 2026 mandates that bank officers seeking higher positions in other banks must pass the Banking Diploma examination, aiming to address the lack of professional competence and reduce reliance on personal connections.

Other Challenges

-

Trade Diversification: Bangladesh’s reliance on trade-related taxes and low trade diversification pose challenges, especially with the imminent graduation from Least Developed Country (LDC) status in 2026, which may affect preferential market access for exports.

-

Illicit Capital Flows: Illicit capital flows deprive the government of revenues. Bangladesh Bank is strengthening anti-money laundering (AML) efforts and coordinating with international partners to recover laundered assets.

-

Climate Change: Bangladesh is particularly vulnerable to the effects of climate change. While not explicitly detailed as a policy response in the search results, the broader context of sustainable development suggests an ongoing focus.

Modernization and Development Initiatives

Bangladesh Bank is actively pursuing modernization and development initiatives to strengthen the financial sector, enhance efficiency, and promote inclusive growth. These efforts are crucial for navigating the evolving financial landscape and achieving national development goals.

Digital Transformation and Financial Inclusion

-

Promoting Digital Banking: We have become increasingly focused on fostering financial inclusion through the promotion of digital banking. This includes encouraging cashless transactions through Mobile Financial Services (MFS) like bKash and Rocket, QR-based payments, and e-wallets, especially for those in rural areas with limited traditional banking infrastructure.

-

Fintech Integration: Bangladesh Bank supports the growth of the fintech industry, ensuring digital payment systems align with international standards. We are embracing fintech and digital solutions to achieve Sustainable Development Goals (SDGs) and the National Financial Inclusion Strategy (NFIS). Initiatives include introducing a Q+ payment app, ERP integration for corporates, streamlining loan processing, and offering Nano loans for micro-financing.

-

Automated Clearing and Settlement: To promote and facilitate financial inclusion, Bangladesh Bank has undertaken comprehensive reforms and upgrades of the country’s financial market infrastructure, including setting up fully automated nationwide online clearing and settlement systems and hastening automation in banks.

-

Green Banking: Bangladesh Bank is the first central bank in the world to issue a “Green Banking Policy,” promoting environmentally responsible financing. This commitment earned its then-governor the title ‘Green Governor’ at the 2012 United Nations Climate Change Conference.

Strengthening Regulatory Framework and Governance

-

Bank Resolution Framework: Bangladesh Bank is working on critical legislative reforms, including the ‘Bank Resolution Act,’ aimed at ensuring long-term stability and good governance in the banking industry.

-

Capacity Building: We are committed to capacity building for the central bank and enhancing human resources. The UK government has pledged continued support for the modernization of Bangladesh Bank into a modern, technology-driven, and robust central bank.

-

Cybersecurity and Fraud Prevention: Efforts include regulating cryptocurrency and blockchain technology to prevent financial fraud and enhancing cybersecurity protocols to protect customers from phishing scams and digital fraud. Digital bank statement verification is also being implemented for visa applications to prevent fraud.

-

FATF Compliance: Bangladesh Bank is actively preparing for the upcoming Financial Action Task Force (FATF) mutual evaluation to ensure Bangladesh’s compliance with global financial security standards.

Supporting SMEs and Underserved Sectors

-

SME Development: To widen and strengthen Small and Medium Enterprises (SMEs), Bangladesh Bank has formed an SME and Special Programs Department. We are detecting hindrances to investment in this sector, especially to help women increase their contribution to industrialization. It has been made mandatory that at least 15% of credit will be disbursed among women entrepreneurs.

-

Agricultural Financing: Bangladesh Bank encourages investments in risky but prospective agro-based/food processing and IT sector projects and provides term finance for infrastructure and other investment projects. We also promote lending to small-holder/tenant farmers and SMEs, with state-owned banks opening millions of new bank accounts with nominal initial deposits to facilitate direct delivery of agricultural input subsidies and social safety net payments.

Frequently Asked Questions (FAQs) about Bangladesh Bank

Here, we address some common questions about Bangladesh Bank and its operations.

Q1: What is the primary objective of Bangladesh Bank’s monetary policy? A1: The primary objective of Bangladesh Bank’s monetary policy is to maintain price stability, stabilize the domestic monetary value, and ensure a competitive external value for the Bangladeshi Taka, thereby fostering economic growth, employment, and development.

Q2: How does Bangladesh Bank promote financial inclusion? A2: Bangladesh Bank promotes financial inclusion by encouraging digital banking services such as mobile banking, e-wallets, and QR-based payments, especially for underserved populations in rural areas. We also support the fintech industry and initiatives like opening low-cost bank accounts for farmers and beneficiaries of social safety nets.

Q3: Who is the current Governor of Bangladesh Bank? A3: Md. Mostaqur Rahman is the incumbent Governor of Bangladesh Bank.

Q4: What is the role of Bangladesh Bank in managing foreign exchange? A4: Bangladesh Bank manages the nation’s foreign exchange reserves and regulates the foreign exchange market to ensure the stability of the Taka in international markets. This is crucial for trade competitiveness and covering import needs and external debt obligations.

Q5: What measures is Bangladesh Bank taking to address non-performing loans (NPLs)? A5: Bangladesh Bank is addressing NPLs through measures such as proposing bank mergers, implementing a Prompt Corrective Action (PCA) framework, undertaking asset quality reviews, dissolving and reconstituting boards of weak banks, and strengthening professional standards for bank officers through mandatory examinations.

Q6: What is the significance of Bangladesh Bank’s “Green Banking Policy”? A6: Bangladesh Bank’s “Green Banking Policy” is significant as it makes us the first central bank globally to issue such a policy, promoting environmentally responsible financing and contributing to sustainable development.

Conclusion: Steering Bangladesh Towards Economic Stability and Growth

Bangladesh Bank stands as a cornerstone of the nation’s economic framework, diligently working to maintain stability and propel growth. Our comprehensive responsibilities, ranging from monetary policy management and currency regulation to financial sector supervision and the promotion of financial inclusion, are vital for the country’s progress. We have actively responded to economic challenges such as inflation and foreign exchange pressures with targeted policy interventions, including tightening monetary policy and implementing exchange rate reforms.

Our commitment to modernization is evident in the push towards digital banking, the integration of fintech solutions, and the continuous efforts to strengthen regulatory frameworks and governance. Initiatives like the “Green Banking Policy” and the focus on supporting SMEs and underserved sectors underscore our dedication to inclusive and sustainable development. As the financial landscape evolves, Bangladesh Bank’s forward-thinking approach remains essential for building a robust, resilient, and equitable financial system, ensuring Bangladesh’s long-term economic stability and success. We are continually striving to enhance transparency and good governance within the financial sector through modern technology.

Merger of Five Islami Banks

In a significant and unprecedented move, Bangladesh Bank has initiated a sweeping consolidation plan to merge five financially distressed Shariah-compliant lenders into a single state-owned entity, tentatively named Sammilito Islami Bank PLC. This intervention marks one of the most substantial regulatory actions in Bangladesh’s Islamic banking sector.

The central bank’s decision, taken at a special meeting of its Board, aims to stabilize the sector amid prolonged liquidity pressures, weak governance, and rising concerns over depositor confidence. The five banks being merged are:

-

First Security Islami Bank

-

Social Islami Bank

-

Union Bank

-

Global Islami Bank

-

EXIM Bank

The merger is a direct response to severe financial distress within these institutions, characterized by alleged fund mismanagement, unauthorized transfers, and alarmingly high non-performing loan (NPL) ratios, reportedly ranging between 70% and 90% at the time of the merger. Such conditions threatened the stability of the entire financial system and eroded public trust.

Key aspects of this merger include:

-

Formation of Sammilito Islami Bank PLC: This newly created bank will absorb the five distressed lenders. Another proposed name for the new entity was “United Islamic Bank”.

-

Capital Structure: The central bank has set an authorized capital of 400 billion Bangladeshi Taka (approximately $3.2 billion) for the merged institution, with paid-up capital fixed at 350 billion Taka (approximately $2.8 billion).

-

Ownership Model: A three-tier shareholding model is being introduced to recapitalize the bank and limit immediate fiscal exposure.

-

The government will inject 200 billion Taka (approximately $1.6 billion) as equity, making it the largest shareholder.

-

75 billion Taka (approximately $611 million) will be raised by converting fixed deposits held by domestic banks and financial institutions within the five merged lenders into shares.

-

Another 75 billion Taka will come from the conversion of fixed deposits belonging to non-bank institutional investors.

-

-

Protection for Retail Savers: Regulators have carved out exemptions to shield sensitive and socially critical entities, ensuring that educational and religious institutions, hospitals, employee provident and gratuity funds, joint ventures, multinational corporations, and foreign diplomatic missions will not be subject to deposit conversion. Retail savers are also guaranteed protection for their deposits. Depositors may be allowed to withdraw up to Tk 200,000.

-

Governance and Management: Bangladesh Bank dissolved the existing boards of the five Shariah-based banks and appointed central bank officials as administrators. Nazma Mobarek, secretary of the Financial Institutions Division under the finance ministry, has been appointed as the new chairman of the board for Sammilito Islami Bank, with seven new directors (five government representatives and two from the private sector). While the new bank will be state-owned, it is intended to be run under private-sector management with market-based salaries for employees and competitive profit rates for depositors.

-

Challenges: The merger faces immense challenges, including the inheritance of a “toxic legacy” with an estimated 77% of combined loans classified as non-performing, operational integration of five distinct IT platforms and corporate cultures, and addressing chronic governance failures.

This consolidation reflects Bangladesh Bank’s urgent attempt to restore oversight, discipline, and stability within a banking sector burdened by corruption, mismanagement, and high levels of non-performing loans. The initiative is a critical step towards preventing a systemic collapse and rebuilding public confidence in the banking system.# Bangladesh Bank: Steering the Nation’s Economic Course

Bangladesh Bank’s Vital Economic Role

Bangladesh Bank, as the central bank of Bangladesh, plays an indispensable role in safeguarding the nation’s financial stability and fostering its economic growth. We recognize its critical responsibility in managing monetary policy, overseeing the banking sector, and shaping the country’s economic future. From stabilizing inflation and managing the national currency, the Taka, to promoting financial inclusion and modernizing banking infrastructure, Bangladesh Bank’s multifaceted functions are central to the nation’s development and global financial integration.

Genesis and Core Responsibilities

Bangladesh Bank was established on December 16, 1971, with retrospective effect, immediately after Bangladesh gained independence. It was formally reorganized under the Bangladesh Bank Order (P.O. No. 127 of 1972) in April 1972, taking over the capital and liabilities of the Dhaka branch of the State Bank of Pakistan. Today, it is fully owned by the Government of Bangladesh.

The central bank’s vision is to continuously evolve as a forward-looking institution with competent and committed professionals, dedicated to monetary management and financial sector supervision. Our mission focuses on maintaining price stability, ensuring financial system robustness, and supporting broad-based, inclusive economic growth, employment generation, and poverty eradication in Bangladesh.

The core functions of Bangladesh Bank are extensive and crucial for a healthy economy:

-

Monetary Policy Formulation and Implementation: Bangladesh Bank is responsible for formulating and implementing monetary policy to stabilize the domestic monetary value and maintain a competitive external value of the Taka. This involves adjusting interest rates and managing the money supply to influence inflation, employment, and overall economic growth. The policy rate currently stands at 10.0%, unchanged since October 2024, with a revised inflation target of “below 8.0%” for FY26.

-

Currency Issuance and Management: We manage the nation’s currency, the Taka, and its interaction with global currencies. This includes issuing currency notes and regulating the foreign exchange market to ensure the Taka’s stability in international markets, which is vital for the country’s export-driven economy.

-

Financial Regulation and Supervision: Bangladesh Bank regulates and supervises scheduled banks and non-bank financial institutions (NBFIs) through off-site and on-site supervision. This is to enhance the safety, soundness, and stability of the banking system, ensure banking discipline, protect depositors’ interests, and maintain confidence in the financial system.

-

Management of Foreign Exchange Reserves: The central bank holds and manages the official foreign exchange reserves, ensuring they are sufficient to cover import needs and external debt obligations. This function is critical for determining currency rates and preventing unexpected inflation.

-

Banker to the Government: Bangladesh Bank acts as the government’s banker, maintaining government accounts and funds, and advising the government on various economic matters.

-

Lender of Last Resort: We serve as a lender of last resort to commercial banks during times of financial crisis, providing liquidity to ensure the stability of the banking sector.

-

Payment System Regulation and Promotion: Bangladesh Bank promotes, regulates, and ensures a secure and efficient payment system, including the issue of banknotes and facilitating inter-bank payments through clearing houses.

-

Financial Inclusion: A significant focus is placed on promoting financial inclusion, encouraging banking services for underserved populations, and supporting digital payment solutions and mobile banking initiatives.

Key Economic Challenges and Policy Responses

Bangladesh’s economy has faced significant challenges in recent years, prompting Bangladesh Bank to implement various policy responses. These challenges include persistently high inflation, a depreciating exchange rate, dwindling foreign exchange reserves, and a growing number of non-performing loans (NPLs) within the banking sector.

Inflationary Pressures

-

Challenge: High and rising prices of essential commodities, particularly food, have been a constant challenge. In July 2024, general inflation significantly increased to 11.66%, with food inflation reaching a record high of 14.10%. This eroded consumer purchasing power, leading to a persistent decline in real wages since mid-2022.

-

Policy Response: To rein in inflation, Bangladesh Bank has consistently tightened monetary policy. This includes introducing an interest targeting framework in FY23 and maintaining a tight monetary condition with a positive real policy rate. The policy rate was maintained at 10.0% since October 2024. Fiscal consolidation efforts, such as expenditure restraint, have also complemented monetary tightening.

Foreign Exchange Reserves and Exchange Rate Volatility

-

Challenge: The country has experienced a decline in foreign exchange reserves and a depreciating Taka, exacerbated by global financial tightening and high international commodity prices. The balance of payments deficit widened, with a significant financial account deficit.

-

Policy Response: Bangladesh Bank has implemented bold exchange rate reforms, including a smooth transition to a flexible exchange rate regime, to address these pressures. We have also tightened control on import flows to manage the reserve decline, although this can impact growth and revenue collection. Efforts are underway to bolster foreign exchange reserve buffers.

Banking Sector Vulnerabilities and Non-Performing Loans (NPLs)

-

Challenge: The banking sector has been struggling with deep-rooted problems, including systemic inefficiencies, weak governance, and a massive accumulation of non-performing loans. Politically motivated appointments, weak internal controls, and ineffective risk management have contributed to these issues. NPLs reportedly rose to around 36% in September 2025, partly due to stricter loan classification rules.

-

Policy Response: Bangladesh Bank has proposed bank mergers and introduced a Prompt Corrective Action (PCA) framework to address these vulnerabilities. We have also taken significant steps, such as dissolving and reconstituting boards of weak banks, undertaking asset quality reviews (AQRs), and initiating mergers of financially distressed institutions. Furthermore, a directive effective from January 2026 mandates that bank officers seeking higher positions in other banks must pass the Banking Diploma examination, aiming to address the lack of professional competence and reduce reliance on personal connections.

Other Challenges

-

Trade Diversification: Bangladesh’s reliance on trade-related taxes and low trade diversification pose challenges, especially with the imminent graduation from Least Developed Country (LDC) status in 2026, which may affect preferential market access for exports.

-

Illicit Capital Flows: Illicit capital flows deprive the government of revenues. Bangladesh Bank is strengthening anti-money laundering (AML) efforts and coordinating with international partners to recover laundered assets.

-

Climate Change: Bangladesh is particularly vulnerable to the effects of climate change. While not explicitly detailed as a policy response in the search results, the broader context of sustainable development suggests an ongoing focus.

Modernization and Development Initiatives

Bangladesh Bank is actively pursuing modernization and development initiatives to strengthen the financial sector, enhance efficiency, and promote inclusive growth. These efforts are crucial for navigating the evolving financial landscape and achieving national development goals.

Digital Transformation and Financial Inclusion

-

Promoting Digital Banking: We have become increasingly focused on fostering financial inclusion through the promotion of digital banking. This includes encouraging cashless transactions through Mobile Financial Services (MFS) like bKash and Rocket, QR-based payments, and e-wallets, especially for those in rural areas with limited traditional banking infrastructure.

-

Fintech Integration: Bangladesh Bank supports the growth of the fintech industry, ensuring digital payment systems align with international standards. We are embracing fintech and digital solutions to achieve Sustainable Development Goals (SDGs) and the National Financial Inclusion Strategy (NFIS). Initiatives include introducing a Q+ payment app, ERP integration for corporates, streamlining loan processing, and offering Nano loans for micro-financing.

-

Automated Clearing and Settlement: To promote and facilitate financial inclusion, Bangladesh Bank has undertaken comprehensive reforms and upgrades of the country’s financial market infrastructure, including setting up fully automated nationwide online clearing and settlement systems and hastening automation in banks.

-

Green Banking: Bangladesh Bank is the first central bank in the world to issue a “Green Banking Policy,” promoting environmentally responsible financing. This commitment earned its then-governor the title ‘Green Governor’ at the 2012 United Nations Climate Change Conference.

Strengthening Regulatory Framework and Governance

-

Bank Resolution Framework: Bangladesh Bank is working on critical legislative reforms, including the ‘Bank Resolution Act,’ aimed at ensuring long-term stability and good governance in the banking industry.

-

Capacity Building: We are committed to capacity building for the central bank and enhancing human resources. The UK government has pledged continued support for the modernization of Bangladesh Bank into a modern, technology-driven, and robust central bank.

-

Cybersecurity and Fraud Prevention: Efforts include regulating cryptocurrency and blockchain technology to prevent financial fraud and enhancing cybersecurity protocols to protect customers from phishing scams and digital fraud. Digital bank statement verification is also being implemented for visa applications to prevent fraud.

-

FATF Compliance: Bangladesh Bank is actively preparing for the upcoming Financial Action Task Force (FATF) mutual evaluation to ensure Bangladesh’s compliance with global financial security standards.

Supporting SMEs and Underserved Sectors

-

SME Development: To widen and strengthen Small and Medium Enterprises (SMEs), Bangladesh Bank has formed an SME and Special Programs Department. We are detecting hindrances to investment in this sector, especially to help women increase their contribution to industrialization. It has been made mandatory that at least 15% of credit will be disbursed among women entrepreneurs.

-

Agricultural Financing: Bangladesh Bank encourages investments in risky but prospective agro-based/food processing and IT sector projects and provides term finance for infrastructure and other investment projects. We also promote lending to small-holder/tenant farmers and SMEs, with state-owned banks opening millions of new bank accounts with nominal initial deposits to facilitate direct delivery of agricultural input subsidies and social safety net payments.

Frequently Asked Questions (FAQs) about Bangladesh Bank

Here, we address some common questions about Bangladesh Bank and its operations.

Q1: What is the primary objective of Bangladesh Bank’s monetary policy? A1: The primary objective of Bangladesh Bank’s monetary policy is to maintain price stability, stabilize the domestic monetary value, and ensure a competitive external value for the Bangladeshi Taka, thereby fostering economic growth, employment, and development.

Q2: How does Bangladesh Bank promote financial inclusion? A2: Bangladesh Bank promotes financial inclusion by encouraging digital banking services such as mobile banking, e-wallets, and QR-based payments, especially for underserved populations in rural areas. We also support the fintech industry and initiatives like opening low-cost bank accounts for farmers and beneficiaries of social safety nets.

Q3: Who is the current Governor of Bangladesh Bank? A3: Md. Mostaqur Rahman is the incumbent Governor of Bangladesh Bank.

Q4: What is the role of Bangladesh Bank in managing foreign exchange? A4: Bangladesh Bank manages the nation’s foreign exchange reserves and regulates the foreign exchange market to ensure the stability of the Taka in international markets. This is crucial for trade competitiveness and covering import needs and external debt obligations.

Q5: What measures is Bangladesh Bank taking to address non-performing loans (NPLs)? A5: Bangladesh Bank is addressing NPLs through measures such as proposing bank mergers, implementing a Prompt Corrective Action (PCA) framework, undertaking asset quality reviews, dissolving and reconstituting boards of weak banks, and strengthening professional standards for bank officers through mandatory examinations.

Q6: What is the significance of Bangladesh Bank’s “Green Banking Policy”? A6: Bangladesh Bank’s “Green Banking Policy” is significant as it makes us the first central bank globally to issue such a policy, promoting environmentally responsible financing and contributing to sustainable development.

Conclusion: Steering Bangladesh Towards Economic Stability and Growth

Bangladesh Bank stands as a cornerstone of the nation’s economic framework, diligently working to maintain stability and propel growth. Our comprehensive responsibilities, ranging from monetary policy management and currency regulation to financial sector supervision and the promotion of financial inclusion, are vital for the country’s progress. We have actively responded to economic challenges such as inflation and foreign exchange pressures with targeted policy interventions, including tightening monetary policy and implementing exchange rate reforms.

Our commitment to modernization is evident in the push towards digital banking, the integration of fintech solutions, and the continuous efforts to strengthen regulatory frameworks and governance. Initiatives like the “Green Banking Policy” and the focus on supporting SMEs and underserved sectors underscore our dedication to inclusive and sustainable development. As the financial landscape evolves, Bangladesh Bank’s forward-thinking approach remains essential for building a robust, resilient, and equitable financial system, ensuring Bangladesh’s long-term economic stability and success. We are continually striving to enhance transparency and good governance within the financial sector through modern technology.

Merger of Five Islami Banks

In a significant and unprecedented move, Bangladesh Bank has initiated a sweeping consolidation plan to merge five financially distressed Shariah-compliant lenders into a single state-owned entity, tentatively named Sammilito Islami Bank PLC. This intervention marks one of the most substantial regulatory actions in Bangladesh’s Islamic banking sector.

The central bank’s decision, taken at a special meeting of its Board, aims to stabilize the sector amid prolonged liquidity pressures, weak governance, and rising concerns over depositor confidence. The five banks being merged are:

-

First Security Islami Bank

-

Social Islami Bank

-

Union Bank

-

Global Islami Bank

-

EXIM Bank

The merger is a direct response to severe financial distress within these institutions, characterized by alleged fund mismanagement, unauthorized transfers, and alarmingly high non-performing loan (NPL) ratios, reportedly ranging between 70% and 90% at the time of the merger. Such conditions threatened the stability of the entire financial system and eroded public trust.

Key aspects of this merger include:

-

Formation of Sammilito Islami Bank PLC: This newly created bank will absorb the five distressed lenders. Another proposed name for the new entity was “United Islamic Bank”.

-

Capital Structure: The central bank has set an authorized capital of 400 billion Bangladeshi Taka (approximately $3.2 billion) for the merged institution, with paid-up capital fixed at 350 billion Taka (approximately $2.8 billion).

-

Ownership Model: A three-tier shareholding model is being introduced to recapitalize the bank and limit immediate fiscal exposure.

-

The government will inject 200 billion Taka (approximately $1.6 billion) as equity, making it the largest shareholder.

-

75 billion Taka (approximately $611 million

-

Md. Mostaqur Rahman FCMA – Governor of Bangladesh Bank

Md. Mostaqur Rahman FCMA officially joined as the 14th Governor of Bangladesh Bank on 26 February 2026, bringing with him more than three decades of professional experience in finance, corporate governance, industrial management, and economic leadership. His appointment marked an important moment for Bangladesh’s financial sector, particularly at a time when the country is focusing heavily on banking reforms, economic resilience, digital transformation, and financial stability.

A highly respected financial professional, Md. Mostaqur Rahman is a qualified Cost and Management Accountant (CMA) and is widely recognized for his expertise in corporate finance, regulatory compliance, capital management, and institutional governance. Over the years, he has built a strong reputation as both a successful entrepreneur and an experienced governance specialist with practical leadership across multiple industries.

Before becoming Governor, Mr. Mostaq played influential roles in several major trade and business organizations in Bangladesh. He served as the Chairman of the BGMEA Standing Committee on Bangladesh Bank, where he worked closely on matters related to export financing, industrial growth, banking coordination, and economic sustainability. His involvement with the ready-made garments (RMG) sector is particularly significant because the industry remains the backbone of Bangladesh’s export economy.

He was also associated with several leading business and professional organizations, including:

| Organization | Role/Association |

|---|---|

| BGMEA | Member and Committee Chairman |

| Chittagong Stock Exchange Ltd. | Member |

| REHAB | Member |

| ATAB | Member |

| DCCI | Member |

These experiences gave him deep exposure to Bangladesh’s industrial landscape, trade environment, investment climate, and financial systems.

Throughout his career, Md. Mostaqur Rahman has demonstrated strong leadership in sectors such as:

- Manufacturing

- Real estate

- Agro-based industries

- Industrial enterprises

- Export-oriented business operations

His work involved strategic financial planning, governance oversight, institutional management, investment supervision, and sustainable business development. Because of this multidisciplinary background, many observers view his appointment as a bridge between the financial sector and the productive sectors of the economy.

In addition to his corporate and institutional achievements, Mr. Mostaq has contributed to policy discussions related to:

- Financial stability

- Industrial financing

- Banking sector governance

- Economic sustainability

- Export competitiveness

Academically, Md. Mostaqur Rahman has a strong educational foundation. He completed his B.Com (Honours) and Master’s Degree in Accounting from the University of Dhaka, one of the country’s most prestigious educational institutions. Later, he earned the professional qualification of Cost & Management Accountant from the Institute of Cost and Management Accountants of Bangladesh (ICMAB).

Born into a respected Muslim family in 1966, he is also known for his involvement in charitable, social welfare, and community development activities. Beyond finance and business, he has maintained a reputation for supporting social responsibility initiatives and community engagement.

As Governor of Bangladesh Bank, Md. Mostaqur Rahman is expected to focus on strengthening banking governance, improving financial discipline, promoting sustainable economic growth, supporting digital financial innovation, and enhancing confidence in Bangladesh’s financial system. His combination of private-sector experience, governance expertise, and economic understanding positions him as a significant figure in the future direction of Bangladesh’s central banking system.