What is Trade Based Money Laundering?

Definition of Money Laundering

What is money laundering?

“Money laundering is the process by which criminals attempt to hide and disguise the true origin and ownership of the proceeds of their criminal activities, thereby avoiding prosecution, conviction and confiscation of the criminal funds.”

UK-Joint Money Laundering Steering Group Guidance Notes

“…any act or attempted act to conceal or disguise the identity of illegally obtained proceeds so that they appear to have originated from legal sources”

INTERPOL definition of Money Laundering as adopted in the General Assembly of 1995

METHODS OF MONEY LAUNDERING

- The use of the financial system (through Cheque or Electronic system);

02) Physical transportation of money (Cash courier)

- Trade Based Money Laundering

- Physical transportation of goods through the trade system.

- Fraudulent Documentation of goods or Services

- Smuggling

TRADE BASED MONEY LAUNDERING

01) Trade-based money laundering is defined as the process of disguising the proceeds of crime and moving value through the use of trade transactions in an attempt to legitimize their illicit origins and to finance objected activities.

02) In practice, this can be achieved through the misrepresentation of the price, quantity or quality of imports or exports.

03) Moreover, trade-based money laundering techniques vary in complexity and are frequently used in combination with other money laundering techniques to further obscure the money trail.

When and why TBML occurs in BD?

International Trade Payment Method

- Advance Payment

- Open Account

- Collection

- Clean Collection

- Documentary Collection

- Document against Acceptance (DA)

- Document against Payment (DP)

- Documentary Letter of Credit

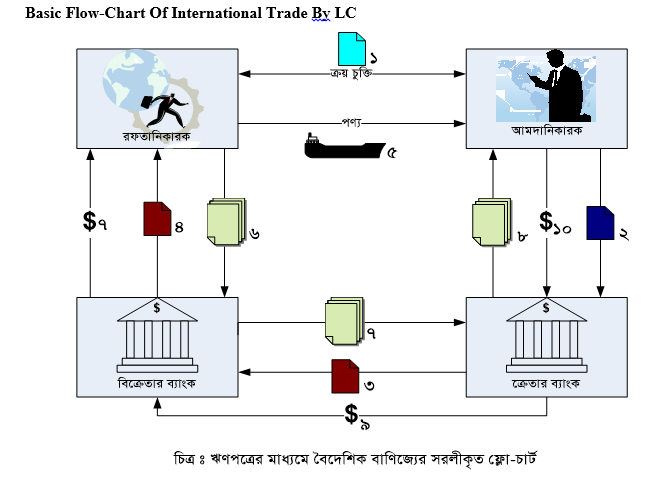

Basic Flow-Chart Of International Trade By LC

Parties Involved

01.Exporter 02.Importer

03.Indenter 04. Buying agent

05.Issuing bank 06.Advising bank

07.Confirming bank 08.Nominated bank

09.Negotiating bank 10.Shipping Co./agents

11.Freight forwarder 12. PSI Co.

13.Customs authority

Legal Aspect of International Trade

The major policies & guidelines that are followed in our country are:

01) Foreign Exchange Regulation Act (FERA)-1947

02) Import and Export (Control) Act-1950

03) Customs Act-1969

04) Importers, Exporters and Indenters (Registration) Order-1981

05) Negotiable Instrument Act-1881

06) Bill of Exchange Act-1882

Under those Acts concerned authorities formulate the followings regulations as per the power conferred upon them:

01) Import Policy order

02) Export Policy

03) Finance Act

04) Customs related SRO

05) FE Circular

07) GFET

There are some international bodies formulating some policy guidelines/rules that are related to International Trade transactions, these are-

01) Uniform Customs and Practices for Documentary Credit (UCPDC)-600

02) Uniform Rules for Collections (URC)-522

03) Uniform Rules for Bank to Bank Reimbursement (URR)-725

04) The Uniform Rules for Demand Guarantee (URDG 458)

05) International Commercial Terms (Incoterms-2000)

06) Documentary Instrument Dispute Expertise (DOCDEX)

07) International Standard Banking Practices, ISBP 2007

Vulnerabilities of TBML

- The enormous volume of trade flows, which obscures individual transactions and provides abundant opportunity for criminal organizations to transfer value across borders;

- The complexity associated with (often multiple) foreign exchange transactions and recourse to diverse financing arrangements;

- The additional complexity that can arise from the practice of commingling illicit funds with the cash flows of legitimate businesses;

- The limited recourse to verification procedures or programs to exchange customs data between countries;

- The limited resources that most customs agencies have available to detect illegal trade transactions.

- Increasing openness of economy.

- There are multiple parties with interconnecting relationships and complicated structures.

- There is no “one size fits all” approach.

- “Dual-use Goods”

Techniques of TBML

- Over- and under-invoicing of goods and services;

- Multiple invoicing of goods and services;

- Over- and under-shipments of goods;

- Short shipment or no shipment (“ghost shipping” or “phantom shipping”).

- Falsely described goods and services.

- Use of Shell or Fictitious Companies.

- Black Market Trades

Over & Under Invoicing-Causes

- Fund flit and Terrorist Financing

- Tax Subsidy

- Policy for Export and Import

- Lack of Data of “Fair Market Price”

- Specialized or complex Product or Services

- Focus on Import rather Export for revenue

- Market Manipulation & abnormal profit making

- Incentives and other privilege

Export: Over Invoicing

Causes of Over Invoicing in Export:

- To get subsidy/cash incentives

- To get CIP status or Export Trophy

- To avail more loan facility than eligibility and divert the fund and ultimately become willful defaulter

- To Repatriate Illegal fund (For Illegal purpose)

- No or less tax on export proceeds (money whitening)

- More dividend facility

Export: Under Invoicing

Causes of under invoicing in export:

1.To use smuggling/drug trafficking or terrorist financing

- To get foreign exchange curb market premium

- Fund flit by both local foreign firms

- Market manipulation by injecting more goods

- Tax evasion

- Dividend deprivation (mainly by Foreign Firms)

Import: Over Invoicing

Causes of Over Invoicing in Import

- Fund flit abroad

- To finance smuggling/drug trafficking/terrorism

03.To terrorist financing

- To get curb market foreign exchange premium

- No or less dividend declaration (foreign Cos)

- Inflate Capital (foreign investment)

O7. Duty draw back facility

- Enhanced Loan facility

Import : Under Invoicing

Causes of under invoicing in import

- Evasion of import duty & tax

- Terrorist financing and smuggling in importing country

03.To use the importing country as dumping station

- To ruin infant/promising/backward linkage industries

- To penetrate in or occupy market for monopoly

- Market manipulation

- Profit inflation

Mechanics of ML through Export & Import

- Collude of Exporter, Importer & Tax Authority

- Sister Concerns (Importer & Exporter of same Group)

- Specialized/complex/antique Product or Services

- Unusual/inconsistent business deal

- Quoted price not consistent with FMV

- High risk commodity deal

- Irrational transportation

- Tax heaven business deal

- Foreign nationals working in Bangladesh

- Foreign business firms operating in Bangladesh illegally;

- Professional bodies/individuals (Doctors, Lawyers, Engineers, Chartered Accountants, etc.)

- Domestic citizens working abroad

Mechanism of over & under invoicing in import & Export

- Over invoicing in export

Sales proceeds + Wages Earners Remittance or other else

- Over Invoicing in import

- In tax-free item like -Capital Machineries.

- Coalition with exporters, PSI Companies and Concerned Officials

- By Foreign Firm/Industries through Back-To-Back LCs

- Import of unusual/ luxurious /antique/complex items

- Under invoicing in export

Coalition with importers, PSI Companies and Concerned Officials

- Under invoicing in import

Coalition with exporters, PSI Companies and concerned Officials

Multiple invoicing of goods and services

- Use of more than one invoice for the same item with deferent FIs

- Responsibility of Advising Bank

- Part Shipment & Any Bank Negotiation

- Responsibility of Negotiating Bank

Over and under shipment

- Shipping Co. or Carrier

- PSI Co.

- Customs Authority

Falsely description of goods and services

- HS Code (Rough Diamond against Semi-processed Diamond

- Software

- Specialized/ Customized Product

- Services

Risk involved regarding TBML and TF

- UN resolution 1267, 1373

- Domestic sanction list;

- Negative news in the Electronic & printing media.

- Correspondent banking

- PEPS

- LIPs

- Financial or political crises

- “Dual-use Goods”

Preventive Measures

- Vulnerable sector and mechanics of ML have to be identified, clarified, focused and monitored.

- Concerned Agencies have to work together

- Review all the legal framework and its implementation

- Identification of backlogs and work together to simplify them.

- Review the activities of all concerned agencies

- Caution in the activities of all concerned FIs and others

- LC issuing bank

- Advising bank

- EXP issuing bank

- Negotiating bank

- Transport Cos

- Customs Authority

- LEAs

- Private Data-base

- Awareness and integrity

- Training & practices

- Safe-guard system introduce

- PSI Certification

- Vigilant about unusual export & import

- Caution against facilitated export & import

- Credit Report

- Reference price

- TTU establishment

Preventive measure: Review of stake holders’ activities

- Customs Agencies

- Law enforcement agencies

- Tax authorities

- Banking supervisions

- Financial Intelligence unit

- Issuing bank

- Advising bank

- Negotiating bank

- PSI Co.

- Shipping Co.

- Analysis of other stake-holders activities

TRADE CONTROL

(a) Institutional / Business-level Risk Assessment

(b) Customer / Transaction-level Risk Assessment

- c) Coverage –methodology for assessing, monitoring and mitigating trade-related activities,

(d) Red Flags

(e) Review and Escalation Procedures of Red Flag Indicators

(f) Exception Reports

(g) Roles and Responsibilities

(h) Documentation

(i) Management Oversight

RED FLAG INDICATORS

- Significant discrepancies appear between the description of the commodity on the bill of lading and the invoice

- Significant discrepancies appear between the description of the goods on the bill of lading (or invoice) and the actual goods shipped

- Significant discrepancies appear between the value of the commodity reported on the invoice and the commodity’s fair market value

- The size of the shipment appears inconsistent with the scale of the exporter or importer’s regular business activities

- The type of commodity being shipped is designated as “high risk” for money laundering activities

- The type of commodity being shipped appears inconsistent with the exporter or importer’s regular business activities

- The shipment does not make economic sense

- The commodity is shipped to (or from) a jurisdiction designated as “high risk” for money laundering activities

- The commodity is transshipped through one or more jurisdictions for no apparent economic reason

- The method of payment appears inconsistent with the risk characteristics of the transaction

- The transaction involves the receipt of cash (or other payments) from third party entities that have no apparent connection with the transaction

- The transaction involves the use of repeatedly amended or frequently extended letters of credit

- The transaction involves the use of front (or shell) companies

- Business involves high risk country’s shipping companies or transit

- Business starts trading with reserved/restricted commodities

- Business issues consciously under or over invoice

- Frequent false description of goods or services

- Export proceeds repatriation from a third country leaning to ML or having a lot of wage earners

- Business with high value/unusual/complex/antique items

- Business with tax haven

- Commercial remittance

AREA OF FOCUS

A review of the current practices of various jurisdictions shows that the following measures can be implemented without hindering legitimate trading activities:

- Applying an intelligence, risk-based and target-based approach which makes consistent use of TBML/FT red flag indicators.

- Using data capture mechanisms such as Electronic Data Interchange (EDI), which is a set of standards for standardizing the structure of information to be electronically exchanged between authorities, from one computer system to another, without human intervention and subject to appropriate data protection safe guards.

- Utilizing the trade data that is gathered automatically from customs declaration forms thereby avoiding any extra burden for the traders who are involved in legitimate trade.

- Having authorizing domestic authorities (e.g. customs, FIU) share information either upon specific request or spontaneously.

- Establishing a Trade Transparency Unit to facilitate the sharing and analysis of import/export data. Because the system does not rely on real-time trade information to target data (the system uses historic data to identify anomalies that are indicative of TBML/FT), legitimate trading activities are not unreasonably hindered.

NEW IDEA-TRADE TRANSPERENCY UNIT (TTU)

- Customs and law enforcement experience has shown that one of the most effective means of analyzing and investigating suspect trade-based activity is to have systems in place that monitor reported imports and exports between countries.

- Consistent with the FATF standards on international cooperation, a number of governments are now sharing import and export information in order to detect anomalies in their trade data.

- To deal with the massive amounts of data generated by such exercises, new technologies have been developed that standardize this information against a range of variables to establish general patterns of trade activity.

- In turn, “trade transparency units” make use of this analysis to identify suspicious trading activities that often merit further investigation.

- The sharing of trade data can be accomplished between cooperating customs authorities through customs mutual assistance agreements.

- The success of such arrangements underscores the importance of cooperating nations working together to establish bilateral mechanisms to detect trade anomalies, which may be associated with money laundering, terrorist financing or other financial crimes.

- Experience shows that trade transparency units create effective gateways for the prompt exchange of trade data and information between foreign counterparts.

- As such, they represent a new and important investigative tool to better combat trade-based money laundering and customs fraud.

Global Compliance Issues

USA: i) Strong and active participation in FATF

- ii) Financial Crime Enforcement Network (FinCEN)

- a) Collects, analyzes and disseminate information

- b) Advisories

- c) Geographic Targeting Orders (GTO)

- d) Special Measures- Monitoring certain FI’s/ExH’s activities, certain type of businesses, etc

iii) Department of Homeland Security’s TTU-Examine trade anomalies and financial irregularities in domestic and foreign trade data (provided by Data analysis and Research for TTU) to identify instances of TBML, customs fraud, contraband smuggling and tax evasion that warrant further law enforcement investigation

iv) Activities of Congress