Intangible Assets -Meaning-Advantage and Disadvantages

What is Intangible Assets:

Intangible Assets: In accounting and law, intangible assets are nonphysical assets or things of value, such as trademarks, patent rights, copyrights (known collectively as intellectual property), franchise rights, leasehold interests, and noncompete agreements, as well as unquantifiable assets often referred to as goodwill or deferred costs, such as corporate culture and strategy, customer satisfaction, and employee loyalty. Although they lack physical substance, intangible assets—also called intangible property—may represent a substantial, or even a major, portion of a company’s total assets.

Intangible assets are usually shown on a company’s balance sheet under noncurrent assets, falling after fixed assets and before or among other assets. Generally they are recorded at their historical cost, and amortized—i.e., gradually written off as expenses over their useful lives. The period of amortization, however, cannot exceed 40 years under the current rules of the Financial Accounting Standards Board. The balance sheet lists such assets only if a company incurs a cost when acquiring them. Hence, non-physical assets acquired without a cost are not included in a company balance sheet. Moreover, not all assets lacking substance are classified as intangible assets. Money owed a company or an account receivable, for instance, is considered a current account, even though it has no substance.

Furthermore, in order for an expenditure to qualify as an intangible asset, a company must expect benefits in the following years and support that expectation with evidence. Expenditures such as those on advertising, for example, may promise future benefits, but the benefits are so uncertain and unpredictable that companies classify them as current expenses.

Read more: https://www.referenceforbusiness.com/encyclopedia/Inc-Int/Intangible-Assets.html#ixzz6IdtcGRdp

The major benefits from the intangible assets are discussed below:

Enhance value of business: Intangible assets play a significant role in enhancing the value of the business. Consumer perception and reputation of the company in the market are the core elements for the success of any company. As the world is largely converting into a global village the importance of the intangible assets like intellectual property, knowledge and business relationships etc are increasing.

Intangible assets are becoming a greater percentage of most of businesses in the recent times as compared to the large space occupying and unnecessary cost incurring intangible assets. However, this concept is relatively new and most of the new businesses on the smaller scale don’t account for these.

They don’t have the adequate understanding of how the company’s reputation or customer base could be beneficial for the company and how to account them properly in the books. Moreover, the more efficiently the intangible assets are managed over the life of the business, the higher the premium earned upon selling the business.

A great Investment: Efficiently managing and accounting for the intangible assets is a form of investment in the business as compared to developing a strong tangible asset base. The company earns a significant premium as compared to the costs incurred in order to acquire, develop or maintain them. Drawbacks and Benefits of Intangible assets

For example, for the tangible asset the company would have to incur the buying / manufacturing cost, storage and maintenance cost, depreciation expense, obsolescence costs etc. While no such costs are born by the company for the intangible assets other than costs which the business has to incur in any case in order to remain in the longer run in the race.

By merely putting all the efforts in enhancing the bottom line of the organization leads to overlooking several other areas of significance. In order to successfully stand out against the competitors in the industry, the company needs to recognize the intangible assets as unique elements. Drawbacks and Benefits of Intangible assets

Intangible assets Drawbacks or Disadvantages are given below:

Going forward, although a strong intangible asset base provides organizations a competitive edge, they also have their drawbacks as well which are explained below: Drawbacks and Benefits of Intangible assets

Complex task: Intangible assets valuation is a complex process and needs core understanding of the various methodologies, approaches and exercises. Often entrepreneurs and booming business don’t have the skills, knowledge and resources to carry out these activities and need expert services from and analyst or accountant. These experts may charge high fees that the company might not be able to bear at the initial phases.

Fraud: Intangible assets can significantly increase the value of a company. The recognition is relatively a newer concept and requires significant developments and rectifications. The management of the company may use creative accounting and window dressing to fraudulently increase the value of the business and earn significant premium on its disposal.

Taxes: Goodwill is reported on the balance sheet under the non-current assets, which is amortized over a time period of no more than 40 years in order to comply with the accounting principles. The company charges amortization on this goodwill periodically on the income statement that reduces the company’s profitability.

Moreover, according to the recent tax regulations the amortization of goodwill is not deductible in the calculation of tax expense payable for the year.

Readmore: https://www.faqifrs.com/drawbacks-and-benefits-of-intangible-assets/

If we start from the fact that financial statements are the primary means of communication between the company and its stakeholders, then the desire of accounting, as a profession is to provide an adequate conceptual Framework, which will enable the preparation of high-quality financial reports, is entirely understandable. According to the IASBs Framework for preparation and presentation of financial statements, providing relevant data about assets, liabilities, equity, income and expenses, other changes of the equity and cash flows will enable achievement of objectives of financial statements. More accurately, by reading and analyzing them, the users will be able to:

get an insight into the history of the company and foresee future performance, presented through future earnings, cash flows, the possibility of fulfilling obligations, perspective in terms of creating added value and the like;

assess the financial structure of the company (financial health of the company) and its exposure to long-term and short-term financial risks;

examine the quality of financial statements presented, in terms of the existence of latent reserves and hidden losses, i.e. to assess to what extent they reflect the economic reality;

carry out a comparative analysis of the company with other possible investors, with the aim of capital allocating to areas of the most profitable use, which contributes to efficient use of resources, encourages investments and stimulates the liquidity of the securities;

discover the ability of the company to adapt to changes on the market of inputs and outputs, to the changes of technology or to resist the competition;

enable early detection of signal on the outlook of the company;

assist the evaluation of company’s ability to service its obligations;

assess the ability of management to create added value [9, p. 23].

Therefore, the information presented in company’s financial statement are important to

users, since they are the basis for making decisions about allocation of resources, which

are always limited. This fact justifies the increased interest of different interest groups for

events in the area of financial reporting in general, and financial reporting on intangible

assets as well. This happens, primarily, for two reasons.

The first reason lies in the fact that, today, the intangible assets are considered to be the key factor of value generating and the potential of growth and development of a company. Based on knowledge, education, organizational and professional experience, motivation of employees, interpersonal relations and the like, intangible assets become the main factor of material form of value creation and the creation of global competition

which in the same time relativises the role of financial and physical capital. The fact is that knowledge has been the main source of long-term economic growth ever since the Industrial Revolution, however, what distinguishes its current meaning, as a generator of growth, is the fact that the information and communication technology accelerated the shift towards a knowledge economy, enabling rapid transmission of information over long

distances at low cost. Certainly, the traditional factors of production have not disappeared, but they have become secondary, i.e. it is considered that intangible assets as an element of business operations, in addition to tangible assets, have a primary contribution to company’s earning power. Success of the company, for the most part, is an effect of the current knowledge, skill, flexibility and management creativity, which is the key element

for gaining the competitive advantage. For these reasons, the information needs of numerous users are directed towards the consideration of a “new” resource of a company,such as internally generated intangible assets, knowledge, relations with stakeholders, organizational culture and the like.

The second reason lies in the fact that the traditional model of financial reporting is fraught with many limitations considering the treatment of intangible assets. Namely, the traditional model of financial reporting allows their presentation in the balance sheet only if they were acquired externally. This way, showing of internally generated intangible investments, i.e. investing in human capital, research and development, advanced technology, relations with customers etc., is absent. So, many categories of intangible assets are not adequately covered by financial statements which caused the market value of many companies, which are knowledge and technology-intense, to be several times lower than the value presented in the balance sheet.

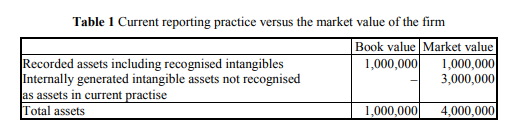

Below, as one illustration, we will demonstrate the relation between book and market value of a company, on the assumption that the book value of the company (the value of tangible assets and externally acquired intangible assets) is set at 1,000,000 $ and market value at 4,000,000 $ [3, p. 67].

The previous table clearly shows that 3,000,000 dinars of the value of the company refers to internally generated intangible assets which could not be recognized or displayed in the balance sheet by the traditional accounting practice. If we look at the relation between the market and book value of the company, i.e. calculate market – to book ratio, we will see that it amounts 4 dinars. This ratio shows that of every 4 dinars of the market

value of the company, only 1 dinar appears in the balance sheet – the remaining 3 dinars refer to internally generated intangible assets of the company.

The situation showed in this way inevitably leads to the conclusion that the traditional model of financial reporting is not able to point to real property, financial or profitable position of a company. As a result, the modification of traditional accounting system, in terms of expanding the possibilities to include the internally generated intangible assets, is inevitable. Namely, the accounting profession is expected not to remain a mere observer of fundamental changes in a modern company. On the contrary, it must actively explore the ways of objective expressing in accordance with accounting principles. The decision makers in the area of financial standards definition are expected to set recommendations for adequate identification of intangible assets elements, a set of criteria for measurement and standards for its disclosure.

Read more: http://facta.junis.ni.ac.rs/eao/eao201003/eao201003-08.pdf